What Is a Secured Credit Card?

A secured credit card is one of the most practical tools for building or rebuilding credit. Here's what it is, how it works, and how to use one to strengthen your credit profile.

If you are new to credit, rebuilding after financial setbacks, or just trying to qualify for your first card, you may have already faced the frustration of being denied when applying for a traditional credit card.

That’s where a secured credit card comes in: it acts as a stepping stone that lets you build your score from the ground up, even if you’ve been turned down before.

What is a secured credit card?

A secured credit card is a real credit card, but it’s backed by a cash deposit you provide upfront. Because this deposit acts as a safety net for the bank, it’s much easier to get approved even if you have no credit history.

In most cases, that deposit becomes your credit limit: if you put down $300, your card typically comes with a $300 credit limit.

From a day-to-day standpoint, it works just like any other credit card. You use it for purchases, receive a monthly statement, and pay the balance. The bank then reports your account activity to some or all of the major credit bureaus (Experian, Equifax, and TransUnion).

The deposit is not the same as prepaying your bill. It is collateral held by the issuer in case you do not pay. You still borrow against a credit line and repay it each month. That distinction matters: a secured card still functions as credit, and using it responsibly is what builds your credit history.

Secured cards usually have high APRs (25%–29%). Always pay your full statement balance; it's the easiest way to avoid interest while building a perfect credit history.

Secured vs. unsecured credit cards

An unsecured credit card is a traditional credit card that does not require a deposit. Approval is based on your credit history, income, and other financial factors. Most of the advertised credit cards fall into this category, including rewards cards, airline cards, and cash back cards. Because unsecured cards carry more risk for the issuer, they are generally only available to people who have already established some credit history.

The easiest way to understand a secured card is to compare it with that kind of traditional card.

| Feature | Secured card | Unsecured card |

|---|---|---|

| Deposit required | Yes | No |

| Helps build credit | Yes | Yes |

| Credit limit | Usually based on your deposit | Based on your credit profile and issuer decision |

| Best for | Building or rebuilding credit | People with established or stronger credit |

Who is a secured credit card for?

Secured cards are designed for people who may not qualify easily for a traditional credit card. That often includes:

- People with no or limited credit history

- People working to recover from past financial setbacks or missed payments

- Students who are just starting to build credit

- People who are new to the country and have income, but little or no local credit file

International students are a perfect fit because credit history typically doesn't transfer between countries. A secured card allows you to build a local credit profile while studying, so you’re ready for the workforce or your next big move with an established history.

In other words, the target is not someone looking for premium travel perks. It is someone who needs a practical, accessible way to demonstrate that they can use credit responsibly, and then use that track record to qualify for better products over time.

How does a secured credit card work?

The process is simple: you provide a refundable security deposit that acts as your credit limit (for example, $300 deposit equals to a $300 limit). You use it like any other credit card, and the issuer reports your payments to the credit bureaus to build your credit score.

The most effective way to use a secured card is to keep things simple:

- Make small, regular purchases such as recurring bills or routine expenses

- Keep the balance low relative to your credit limit (aim for under 10%)

- Always pay on time to build a perfect payment history

- Pay the full balance monthly to avoid high interest charges

That consistent pattern is what builds a positive credit history over time.

How does a secured card help build credit?

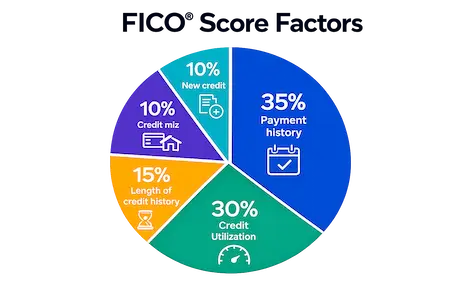

A secured card helps build credit because it creates a documented track record. When the issuer reports your account to the credit bureaus, it contributes to several of the factors that make up your FICO score.

Here is how a secured card touches each one:

Payment history (35%) is built one month at a time. Every on-time payment is reported to the credit bureaus, and a consistent record of paying on time is the single most effective thing you can do to improve your score over the long term.

Credit utilization (30%) is the percentage of your available credit that you are using. If your credit limit is $300 and your current balance is $90, your utilization is 30%. Keeping this number at or below 30%, and ideally below 10%, signals responsible credit management to lenders. On a $300 limit, that means keeping your balance under $30 at statement time.

Length of credit history (15%) rewards accounts that have been open and active over time. The longer your account has been in good standing, the more positively it contributes to this factor. This is one reason it might be worth keeping a secured card open even after you qualify for a better product.

Credit mix (10%) reflects the variety of credit types on your report, such as revolving accounts (like credit cards) and installment loans (like a car loan or student loan). A secured card adds a revolving account to your file.

New credit (10%) accounts for recent credit inquiries and newly opened accounts. Applying for a secured card may result in a temporary small dip in your score if the issuer runs a hard inquiry, but this effect is short-lived, and the long-term benefit of building credit far outweighs it.

A secured card only works as a credit-building tool if the issuer reports to the bureaus. Before applying, confirm that the card reports to all three: Experian, Equifax, and TransUnion.

What benefits can a secured card offer?

The main benefit of a secured card is not rewards. It is access. It gives you a way to start building credit when other products may be out of reach, and stronger credit can make it easier later to qualify for better cards, loans, apartment rentals, and lower borrowing rates.

Some secured cards also offer:

- A path to upgrade to an unsecured card after a period of responsible use

- The return of your deposit when you graduate or close the account in good standing

- Basic rewards or cash back on everyday purchases

Those should be viewed as secondary. The primary goal is building a stronger credit history, and the card that best supports that goal is the one you will use consistently and pay reliably, not necessarily the one with the most features.

Bottom line

A secured credit card is one of the most practical first steps for anyone who needs to build or rebuild credit. Used consistently and paid in full each month, it creates the credit profile that opens the door to better rates, better cards, and eventually the kind of rewards that make travel more accessible.